Understanding Pension Rights After Termination in 2024

This comprehensive guide explores the impact of job termination on pension benefits, detailing the differences between defined benefit and defined contribution plans, vesting periods, and options for taking lump-sum payments or rolling over funds to an IRA.

Abhinil Kumar

Author

In today’s uncertain job market, one of the biggest concerns for many employees revolves around the security of their pension benefits if they were to unexpectedly lose their job. Understanding what happens to your pension when you get fired is crucial for planning your financial future and ensuring that you are prepared for any changes in your employment status. This comprehensive guide will explore various aspects of pension plans, including the impact of termination on your retirement benefits, and will provide essential advice for safeguarding your financial well-being.

Understanding Your Pension Plan

A pension plan is a type of retirement plan typically provided by employers that offers you a guaranteed income after retirement. The specifics of each plan can vary widely, but they generally fall under two categories: defined benefit plans and defined contribution plans. Defined benefit plans, often referred to simply as pension plans, promise a specified monthly benefit at retirement, often based on factors like your salary, age, and length of employment.

Types of pension plans:

There are two main types of pension plans: defined benefit and defined contribution.

1. A defined benefit pension plan is one in which the payout during retirement is determined by a formula that takes into account various factors such as salary scale, years of service, and age. The employee receives a predetermined payout for life, regardless of the performance of the investments made with the funds contributed to the plan. This type of pension is often seen as more secure, as the retiree has a guaranteed income for the rest of their life.

2. On the other hand, a defined contribution plan is one in which the retirement payout depends on the performance of the investments made with the funds contributed to the plan. The employer and/or employee make contributions to the plan, and these funds are invested in various assets such as stocks, bonds, and mutual funds. The final payout depends on how well these investments perform over time. This type of pension plan carries more risk, as the retirement income is not guaranteed and depends on the performance of the investments.

It is important to note that defined benefit pensions are often non-transferable, meaning that they cannot be transferred to another pension scheme or plan. In contrast, defined contribution pensions can be transferred to another scheme or plan if desired. However, transfers of defined benefit pensions over $40,000 typically require independent financial advice to ensure that the individual fully understands the implications and potential risks involved in transferring their pension.

What Happens to Your Pension If You Get Fired?

When you are terminated from your job, the fate of your pension benefits can differ based on the type of plan and the terms specified within your pension plan documents. Here are some key factors to consider:

- Vesting Period: Most pension plans have a vesting period, which is the time you need to work at the company to earn the right to benefits from the plan. If you are vested in the pension plan, you generally retain the rights to your benefits, regardless of whether you are fired or you quit.

- Non-Vested Benefits: If you are not vested in the pension plan when you are terminated, you may lose your accrued benefits entirely. This makes understanding your plan’s vesting schedule and your own vesting status critical.

- Lump-Sum Payment vs. Monthly Payments: Some plans may offer the option to take your pension as a lump-sum payment instead of receiving monthly payments upon retirement. If you are terminated, taking a lump-sum payout might be beneficial or necessary, depending on your financial situation.

- Pension Plan Type: The type of pension plan you are enrolled in can also affect what happens if you get fired. For example, if you have a contribution plan like a 401(k), your contributions are generally vested immediately, and you retain all your benefits. However, employer contributions might have a different vesting schedule.

Vesting Period and Termination of Employment

The vesting period refers to the duration of time that an employee must work for a company before they are fully entitled to the benefits of a retirement plan or other types of employee benefits. It is designed to encourage employee loyalty and reward long-term commitment to the organization.

When it comes to termination of employment, the vesting period is crucial. If an employee terminates their employment before the vesting period is complete, they may not be entitled to the full benefits of the retirement plan. Instead, they may only receive a portion of the benefits based on the number of years they have completed within the vesting period.

Requirements and regulations regarding vesting in a retirement plan can vary depending on the specific plan and the company offering it. However, there are typically federal regulations that outline minimum vesting requirements to protect employees. The Employee Retirement Income Security Act (ERISA) sets these standards for retirement plans, ensuring that employees have the opportunity to accrue vested benefits over time.

Several factors can affect vesting, including the company’s vesting schedule, the employee’s length of service, and any additional requirements or provisions outlined in the retirement plan. These factors can impact the amount of benefits an employee is entitled to upon termination. For example, if a company has a five-year vesting schedule and an employee terminates their employment after only three years, they may only be entitled to 60% of the benefits they have accrued.

Forfeitures are another important aspect to consider in relation to termination and vesting. When an employee terminates their employment before becoming fully vested, any unvested portion of their benefits is typically forfeited. These forfeitures are then usually distributed back into the retirement plan to benefit the remaining participants.

Impact of termination of employment on vesting period

When an individual’s employment is terminated, the vesting period for their retirement plans can be directly impacted. Vesting refers to the process in which an employee becomes entitled to the employer’s contributions made towards their retirement benefits, often over a specified period of time.

- Forfeiture of Contributions:

- If an employee is not vested in their retirement plan upon termination, they may forfeit the employer’s contributions.

- Cliff Vesting Schedule:

- Employees become fully vested after a set number of years of service (typically three to five years).

- If terminated before reaching the required years, the employee may lose all employer contributions.

- Graded Vesting Schedule:

- Employees become partially vested after a certain period and continue to gain more vesting over time.

- If terminated before full vesting, the employee is entitled only to a portion of the employer’s contributions.

- Options Post-Termination:

- Employees may have the option to cash out or transfer the value of their pension plan to another retirement account.

- These options can be influenced by factors such as the employee’s age, length of employment, and specific provisions of the pension plan.

Lump sum payment options

When it comes to receiving a lump sum pension payment, various options are available, and understanding the potential tax implications and the importance of financial planning is crucial.

One option is to receive the entire lump sum payment in cash. While this may seem tempting, it is important to consider the tax implications of this choice. A lump sum payment is generally taxable as ordinary income, which means it could push you into a higher tax bracket. This could result in a significant tax bill that can be overwhelming if not properly planned for.

Another option is to roll the lump sum payout into an Individual Retirement Account (IRA). By doing so, you can avoid immediate taxes and maintain tax-deferred growth. This means that you can continue to grow your investment without needing to pay taxes on the earnings until you start making withdrawals.

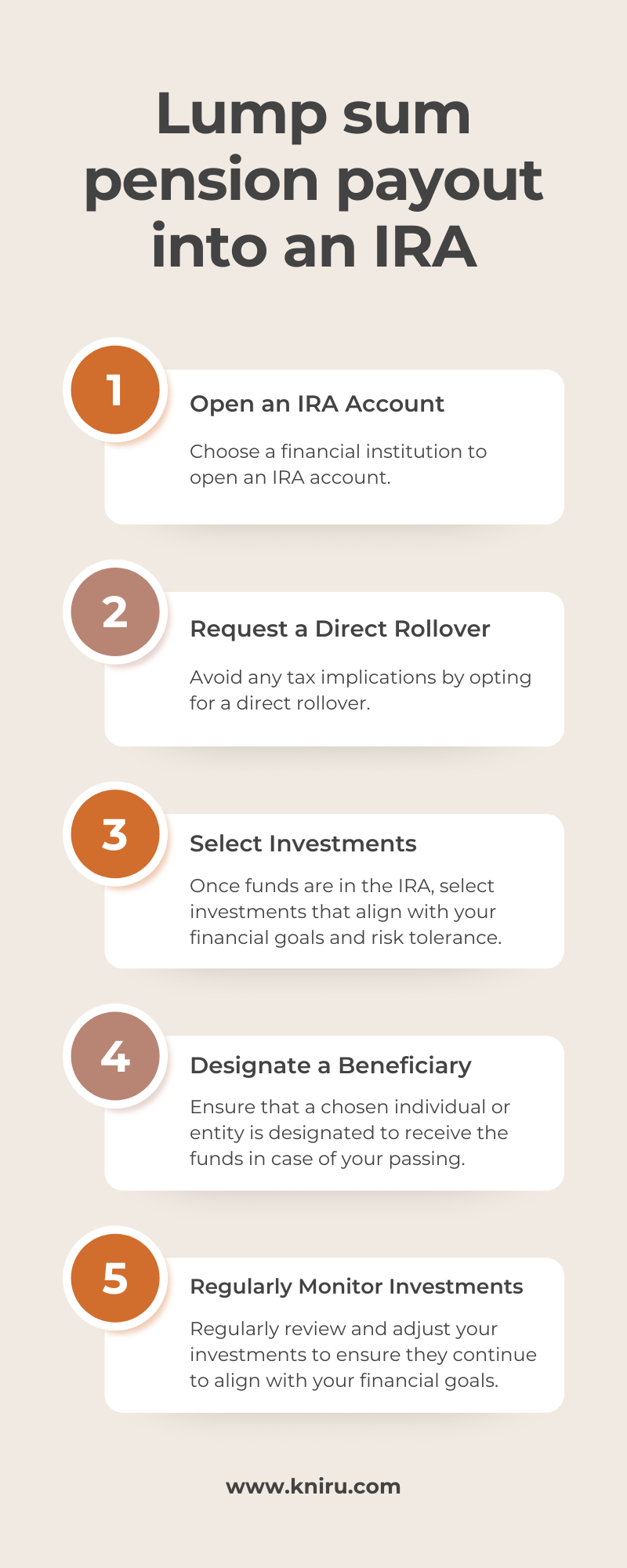

To roll the lump sum pension payout into an IRA, there are several steps involved.

- Open an IRA Account:

- Choose a financial institution to open an IRA account.

- Request a Direct Rollover:

- Ensure funds are transferred directly from your pension plan to the IRA.

- Avoid any tax implications by opting for a direct rollover.

- Select Investments:

- Once funds are in the IRA, select investments that align with your financial goals and risk tolerance.

- Designate a Beneficiary:

- Ensure that a chosen individual or entity is designated to receive the funds in case of your passing.

- Regularly Monitor Investments:

- Regularly review and adjust your investments to ensure they continue to align with your financial goals.

Lump sum payment options

Rolling over funds to an IRA or new employer’s plan

Rolling over funds to an IRA or new employer’s plan is a process that allows individuals to transfer their retirement savings from an old plan to a new one. There are several options available when rolling over funds, each with its own tax implications.

One option is to roll over the funds into an Individual Retirement Account (IRA). This allows individuals to maintain control over their retirement savings and take advantage of the tax benefits that IRAs offer. Another option is to roll over the funds into a new employer’s retirement plan, if available. This option allows individuals to continue saving for retirement with their new employer and potentially receive any employer -matching contributions.

Consolidating retirement savings into one account has several benefits. Firstly, it allows for easier tracking of the funds and simplifies the management of investments. Rather than keeping track of multiple accounts, individuals can monitor their retirement savings in one place. Additionally, consolidating funds can potentially lower fees and administrative costs associated with maintaining multiple accounts.

The process of rolling over funds can be done through a direct transfer or by requesting a lump-sum distribution. With a direct transfer, the balance from the old plan is directly transferred to the new plan or IRA, avoiding any tax implications. With a lump-sum distribution, the individual receives a check for the balance and has 60 days to deposit it into a new plan or IRA. If not deposited within 60 days, taxes and penalties may apply.

Immediate Options After Termination

After termination, an employee has several immediate options to consider.

- Severance Agreement:

- Consider entering into a severance agreement with the employer.

- May include a financial package providing compensation for loss of employment.

- Could also include benefits such as outplacement services or continuation of certain employee benefits for a specific period.

- Health Care Coverage Under COBRA:

- COBRA allows terminated employees to maintain health insurance coverage.

- Terminated employees may need to pay the full cost of the coverage themselves.

- Essential for individuals with ongoing medical needs or those bridging the gap until securing new employment with health benefits.

- Defined Benefit Pension Options:

- Decide whether to take a lump sum payment or opt for regular payments in the future.

- Decision depends on the individual’s age and years of retirement.

- Lump Sum Payment vs. Regular Payments:

- Younger Employees:

- Taking a lump sum payment and investing it may be appealing for potential growth over time.

- Older Employees Nearing Retirement:

- Regular payments may provide a steady income stream during retirement years.

- Younger Employees:

Financial Advice for Managing Pension After Termination

Losing a job can be a stressful experience, especially when you are concerned about your financial future. Here are some strategies to manage your pension effectively:

- Consult a Financial Advisor: A financial advisor can offer personalized advice tailored to your specific financial situation and help you understand the complexities of your pension plan.

- Review Your Pension Plan Documentation: Make sure you understand all the aspects of your pension plan. Review the pension plan documents carefully or request a copy from your pension plan administrator if necessary.

- Consider the Tax Implications: Whether you decide to take a lump-sum distribution or continue receiving monthly payments, each choice has different tax implications. Consulting with a tax advisor can help minimize potential tax liabilities.

Conclusion

Understanding what happens to your pension if you get fired is essential for every employee. By familiarizing yourself with the details of your pension plan and seeking professional advice, you can make informed decisions that protect your retirement savings and ensure financial stability, no matter what changes come your way in your career.

Remember, each pension plan has unique features, and the terms can vary significantly from one employer to another. Always stay proactive about understanding your benefits and seek clarity on any points that might impact your future financial security.

FAQs

Q1: What happens to my pension if I get fired? When you get fired, the status of your pension depends on the type of pension plan you have and whether you are vested. If you are vested, you generally retain the rights to your pension benefits. If you are not vested, you may lose the benefits accrued. It’s important to check your specific pension plan documents to understand the exact terms.

Q2: What does it mean to be vested in a pension plan? Being vested in a pension plan means you have earned the right to receive benefits from the plan, even if you leave the employer. The vesting period varies by plan, but it typically requires you to work for a certain number of years before you are fully vested.

Q3: Can I take a lump-sum payment from my pension if I get fired? Some pension plans offer the option to take your pension as a lump-sum payment instead of monthly payments upon retirement. This can be beneficial or necessary depending on your financial situation after termination. Check your pension plan documents to see if this option is available to you.

Q4: What are the tax implications of taking a lump-sum pension payment? Receiving a lump-sum pension payment can have significant tax implications, as it is generally taxed as ordinary income. This could potentially push you into a higher tax bracket, resulting in a substantial tax bill. Consulting with a tax advisor can help you understand and manage these implications.

Q5: What should I do with my defined contribution plan if I get fired? If you have a defined contribution plan like a 401(k), you have several options. You can leave the funds in your current plan, roll them over to an Individual Retirement Account (IRA), or transfer them to a new employer’s retirement plan. Each option has different benefits and potential tax implications, so it’s advisable to consult with a financial advisor to make the best decision for your situation.