What Happens to Stock Options After You Leave a Company in 2024?

Stock options are financial tools that give employees the right to buy or sell company stock at a set price within a specified timeframe, aligning their interests with company goals. This guide details what happens to your stock options after leaving a company, the impact of different stock option types, and the tax implications involved. Understanding these factors is crucial for making informed financial decisions and maximizing the benefits of your stock options.

Abhinil Kumar

Author

Stock options are financial instruments that give individuals the right to buy or sell stocks at a predetermined price within a specified timeframe. They are often given to employees as a motivation tool, helping to align their goals with the company’s objectives.

The purpose of stock options, particularly employee stock options, is to align the interests of employees with those of the company. By giving employees the opportunity to become shareholders, they have a vested interest in the company’s success. This can motivate employees to work harder and contribute to the long-term growth of the organization.

In terms of specific types of employee stock options, there are two commonly used categories: incentive stock options (ISO) and non-qualified stock options (NSO). The main difference lies in their tax treatment. ISOs receive special tax treatment, where employees are not subject to immediate tax upon exercise or sale of the options. However, they may be subject to the alternative minimum tax. On the other hand, NSOs are subject to regular income tax upon exercise, based on the difference between the market price and the strike price at the time of exercise.

Importance of understanding stock options after leaving a company

Understanding stock options is crucial for individuals who have recently left a company. Stock options, which are a form of compensation commonly provided by employers, grant employees the right to buy company stock at a predetermined price in the future. These options can be a valuable asset for employees, as they have the potential to generate significant financial gains. However, without a comprehensive understanding of stock options and their associated implications, individuals may find themselves missing out on potential benefits or making uninformed decisions. Therefore, gaining insight into how stock options work and how they can be leveraged effectively is essential for those who have recently transitioned away from a company. This understanding empowers individuals to make informed financial decisions, maximize the value of their stock options, and take advantage of their potential benefits to secure their financial future.

What Happens to Your Stock Options After Leaving a Company?

1. Vesting of Stock Options Upon leaving a company, the status of your stock options hinges critically on the vesting schedule. Typically, stock options vest over a set period of time, which can range from immediate vesting to plans extending over several years. Understanding your company’s specific vesting period is paramount. If your options have vested before your departure, you generally have the right to exercise them within a defined window, often ranging from 30 to 90 days after termination.

2. Unvested Stock Options: For options that have not yet vested at the time of your departure, the common practice is forfeiture. However, some companies may offer provisions under certain conditions such as retirement, disability, or other special circumstances where unvested options could continue to vest or accelerate.

3. Exercise Price and Strike Price Understanding the exercise or strike price of your stock options is crucial. This price is typically set at the market price of the company’s stock when the options are granted. If the company’s stock has increased in value, exercising your options to buy at the lower grant price could offer significant financial benefit.

4. Tax Implications The taxation of stock options can be complex:

- At Exercise: For NSOs, the spread between the exercise price and the market value at exercise is taxed as ordinary income.

- At Sale: For ISOs, if shares are held for the required period, gains are taxed as long-term capital gains. If not, they are treated as ordinary income.

Types of Stock Options

There are four main types of stock options: ISOs (Incentive Stock Options), NSOs (Nonqualified Stock Options), RSAs (Restricted Stock Awards), and RSUs (Restricted Stock Units).

- ISOs are typically granted to employees and have specific tax advantages. They are only available for employees and cannot be granted to contractors or consultants. ISOs have certain restrictions, such as a maximum grant value of $100,000 per year per individual.

- NSOs, on the other hand, can be granted to employees, contractors, consultants, and directors. They do not have the same tax advantages as ISOs and are taxed as ordinary income when exercised.

- RSAs are actual shares of stock that are granted to an employee up front. These shares are subject to certain restrictions and vesting conditions, which means the employee may not have full ownership of the stock until a certain period of time has passed or specific performance goals have been met.

- RSUs are similar to RSAs, but instead of receiving actual shares, employees are granted units that represent the right to receive shares in the future. Like RSAs, RSUs are subject to vesting conditions and performance goals.

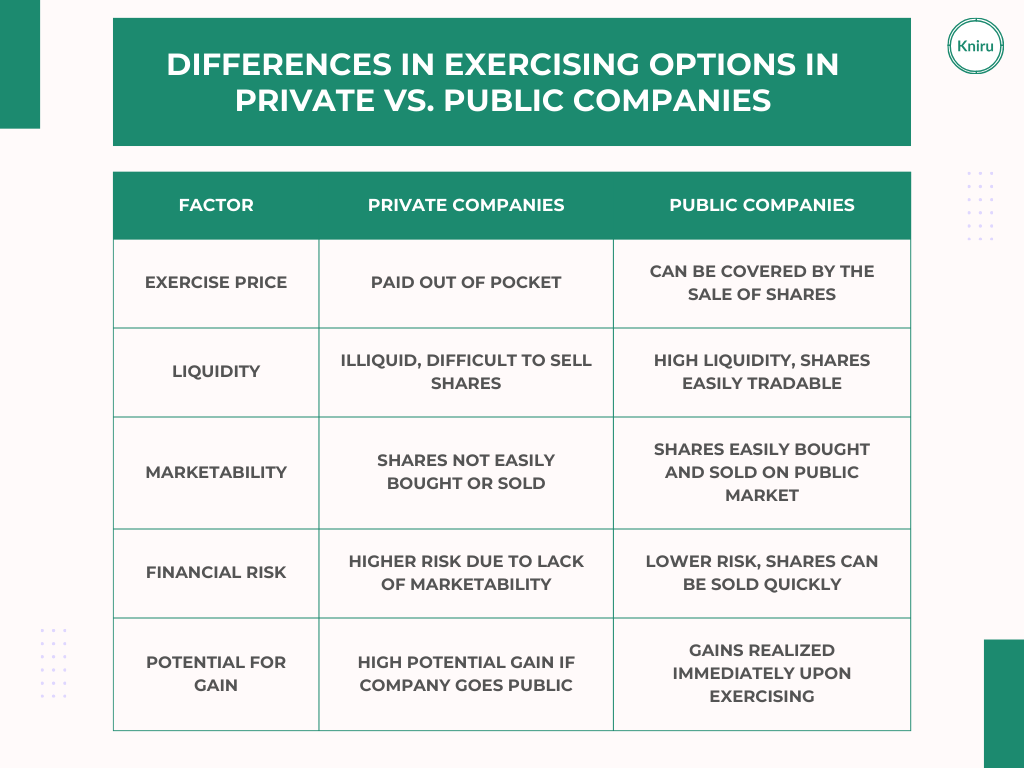

Differences in exercising options in Private vs. Public companies

Exercising stock options in private and public companies differ significantly in terms of accessibility, funding, and liquidity. In private companies, the process requires the employee to pay out of pocket to exercise and fund the purchase, whereas in public companies, employees can often exercise their options without any immediate financial burden.

When it comes to private companies, employees must typically pay the exercise price, which is usually set at the fair market value of the stock at the time of grant. Unlike public companies, where the exercise price can be covered by the sale of the shares, employees in private companies have to fund the purchase using their personal finances. This can be a substantial financial commitment, especially if the exercise price is high.

One notable risk of holding onto illiquid shares in private companies is the lack of marketability. Unlike publicly traded stocks, shares in private companies are not easily bought or sold. As a result, employees may find it difficult to convert their shares into cash. Additionally, there is a risk that the value of the shares may decline or become worthless. This lack of liquidity can limit employees’ ability to access their funds and can potentially lead to financial challenges.

However, exercising stock options in private companies can have advantages when the company files for an initial public offering (IPO). Once a private company goes public, its shares become tradable on a public stock exchange, providing employees with the opportunity to sell their shares and potentially realize a substantial financial gain. This liquidity event can significantly enhance the value of the stock options.

Differences in exercising options in Private vs. Public companies

Considerations for Private Companies

When it comes to exercising incentive stock options (ISOs), private companies need to carefully consider several factors to ensure they make the most of this opportunity.

First and foremost, private companies must evaluate the risk of holding illiquid shares. Unlike publicly traded companies, private companies may not have an active market for their shares, making it difficult for employees to sell their ISOs. This lack of liquidity could restrict an employee’s ability to realize the value of their options.

Private companies should also consider the potential timing of an initial public offering (IPO). Going public can provide liquidity for employees, allowing them to sell their shares. Therefore, employees should exercise options strategically, considering IPO plans and the resulting increase in stock value.

Another important consideration is the holding period requirements for favorable tax treatment. ISOs grant employees the opportunity to be taxed at long-term capital gains rates instead of higher ordinary income rates. However, to qualify for this benefit, employees must hold the shares for at least one year from the exercise date and two years from the grant date.

Private companies should also account for the lock-up period after listing. During this period, employees are prohibited from selling their shares, which could impact liquidity and the ability to convert shares into cash.

Lastly, companies must coordinate the exercise of ISOs with eligibility requirements for preferential tax treatment. Employees need to ensure they meet all the criteria, such as being an employee of the company and not exceeding the $100,000 limit for ISOs exercisable in any calendar year.

Valuation challenges for private company stock options

Valuation challenges for private company stock options can be complex and often require careful consideration. Unlike publicly traded stock options, which have readily available market prices, valuing private company stock options can be more subjective and can involve a range of factors. In this article, we will explore the key challenges that arise when valuing private company stock options and examine the techniques commonly used to overcome these challenges. Understanding the intricacies involved in valuing private company stock options is crucial for both companies that offer these options to employees and individuals who hold them, as it directly impacts their financial decisions and potential returns.

Conclusion

Understanding the implications of leaving a company with unexercised stock options is crucial for any employee participating in equity compensation plans. Whether you hold Incentive Stock Options or Non-Qualified Stock Options, the decisions you make can have significant financial and tax implications. It’s important to consult with financial advisors to navigate the complexities of option agreements, strike prices, and the vesting period. Employees should be aware of the post-termination exercise window and any potential tax liability associated with exercising their options or when their shares vest. Companies often use these stock options as a part of a broader compensation package, providing financial advisors as resources to ensure employees understand their options and the best strategies for their personal financial goals. Remember, each type of equity compensation, from phantom stock to restricted stock units, comes with its own set of rules and tax treatments, which can impact your financial planning and the timing of exercising your options.

FAQ

- Can I exercise my vested stock options after I leave the company? Yes, employees generally have a post-termination exercise window to exercise their vested options. This window usually ranges from 30 to 90 days after termination, but it’s crucial to check your specific stock option grant for details.

- Are there tax implications when exercising stock options after leaving a company? Exercising stock options can lead to tax liabilities, including income tax on the bargain element of non-qualified stock options. Incentive stock options may have favourable tax treatment if certain conditions are met. Always consult with a tax advisor for guidance based on your personal situation.

- What should I consider before exercising my stock options? Consider factors like the current market price of the shares compared to your strike price, potential tax implications, and your personal financial goals. Discussing your options with a financial advisor can provide clarity on the best timing and strategies for exercise.

- How do different types of stock options impact my decisions after leaving a company? The type of stock options you hold—whether non-qualified or incentive—can affect your financial planning. Each type has different rules regarding taxation, exercise periods, and eligibility for favourable tax treatments, which should be considered in your decision-making process.